June 2026•Nidhi Adwani

Which ITR form should I file? ITR filing 2025-26

Every year, millions of Indian taxpayers ask one urgent question as the deadline approaches: Which ITR form should I file? Get it wrong, and you’re looking at a defective return notice, penalties, or worse a scrutiny assessment from the Income Tax Department. With ITR filing 2025-26 season now open, choosing the right form ITR 1, ITR 2, ITR 3, or ITR 4 is more critical than ever. This guide breaks it all down, clearly and completely.

hether you are a salaried professional earning from a single employer, a business owner with multiple income streams, or a freelancer opting for the presumptive tax scheme, the correct ITR form determines the validity of your income tax return 2025-26. Filing the wrong form is treated as a non-filing by the Income Tax Department of India, and that carries serious consequences. This blog is your definitive resource for understanding ITR 1 vs ITR 2 vs ITR 3 vs ITR 4. For a quick comparison table, also

See our detailed guide: ITR 1 vs ITR 2 vs ITR 3 vs ITR 4 : Complete 2025 Comparison

Why Choosing the Correct ITR Form Matters for ITR Filing 2025-26

The Income Tax Department processes over 8 crore returns annually. According to guidelines issued by the Central Board of Direct Taxes (CBDT), filing an incorrect ITR form renders the return defective under Section 139(9) of the Income Tax Act. The assessee is then given 15 days to correct and re-file but during this window, refunds are held, and interest on outstanding tax continues to accrue.

Dr. Haresh Adwani, Ph.D. in Commerce and a Law Graduate with over a decade of tax advisory experience at Adwani and Company, explains it plainly: “Most errors I see in practice are not calculation errors they are form-selection errors. A taxpayer with capital gains blithely files ITR 1, which doesn’t accommodate that income. The return is flagged before processing even begins.”

Getting your ITR filing 2025-26 right from the start saves you time, avoids notices, and ensures your refund reaches you faster.

What’s New in ITR Filing 2025-26? Key Changes You Must Know

Before diving into form eligibility, it’s worth noting the changes effective for Assessment Year (AY) 2026-27, i.e., income earned in Financial Year 2025-26:

- The new tax regime is now the default regime for all individuals. If you wish to opt for the old regime with deductions (80C, 80D, HRA, etc.), you must explicitly select it while filing.

- The basic exemption limit under the new regime has been revised upward to ₹3,00,000, with a full rebate under Section 87A available for incomes up to ₹7,00,000.

- The Annual Information Statement (AIS) and Taxpayer Information Summary (TIS) on the Income Tax e-filing portal (incometax.gov.in) now reflect near-real-time data from banks, registrars, and mutual funds. Mismatches trigger auto-scrutiny.

- TDS rates on several categories of payments have been revised, impacting Form 26AS reconciliation for ITR filing 2025-26.

These changes make accurate form selection even more important this assessment year. The team at Adwani and Company stays current with every CBDT circular and Finance Act amendment so that clients are never caught off guard.

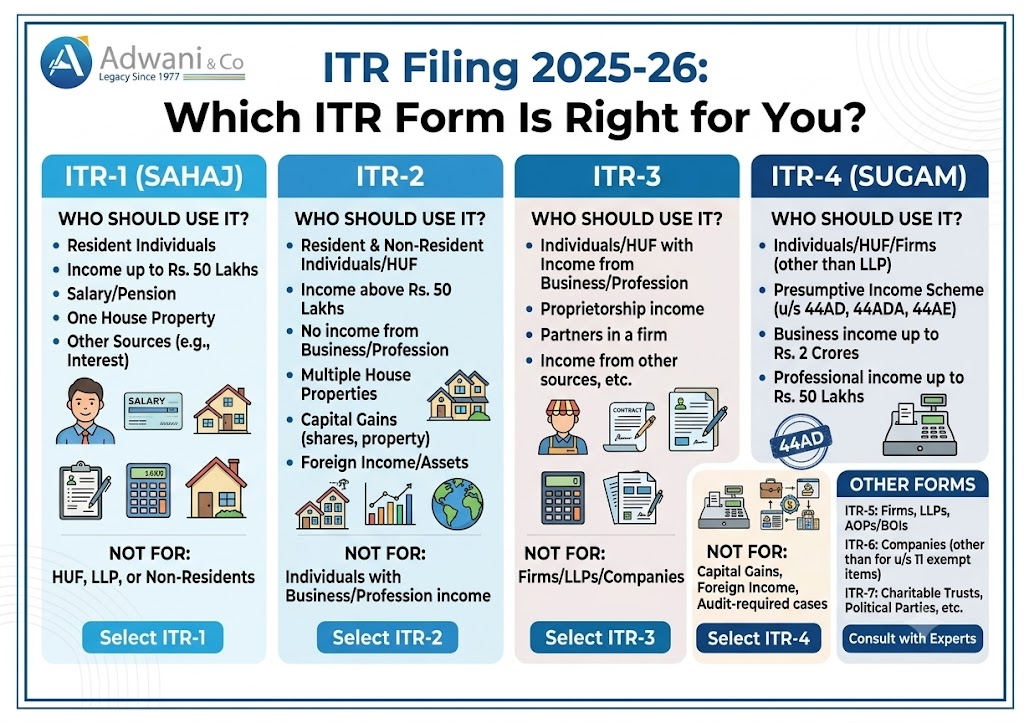

ITR 1 (Sahaj): The Simplest Form for ITR Filing 2025-26

Who Can Use ITR-1?

ITR 1, popularly called Sahaj (meaning “easy” in Hindi), is designed for resident individuals with straightforward income profiles. For ITR filing 2025-26, you can use ITR 1 only if ALL of the following conditions are met:

- Total income does not exceed ₹50 lakh

- Income is from salary or pension only

- Income from one house property (no brought-forward losses)

- Income from other sources such as savings bank interest, FD interest, family pension

- Agricultural income up to ₹5,000

Who CANNOT Use ITR 1?

- If you have income from capital gains (short-term or long-term)

- If you are a Director in a company

- If you hold unlisted equity shares

- If you have foreign assets or foreign income

- If TDS has been deducted under Section 194N (cash withdrawals above threshold)

- If you have income from business or profession

Practical Example: Ramesh Sharma is a government school teacher earning ₹8.4 lakh per annum. He has a savings bank account earning ₹12,000 in interest and owns one self-occupied flat. He has no capital gains, no foreign assets, and no business income. Ramesh can correctly file ITR 1 for ITR filing 2025-26.

Learn more about our: Income Tax Filing for Salaried Individuals: A Complete Guide for AY 2026-27 and let Adwani and Company handle your return end-to-end.

ITR 2: For Capital Gains, Multiple Properties & Foreign Income

Who Should File ITR 2 in 2025-26?

ITR 2 is for individuals and Hindu Undivided Families (HUFs) who do NOT have income from business or profession, but whose income profile is more complex than ITR 1 allows. Use ITR 2 for income tax return 2025-26 if you have:

- Income exceeding ₹50 lakh

- Capital gains from sale of property, equity shares, mutual funds, gold, etc.

- Income from more than one house property, or any house property with carried-forward losses

- Foreign income or foreign assets (including NRI taxpayers)

- You are a Director of a company or hold unlisted equity shares

- Agricultural income exceeding ₹5,000

- Winnings from lottery, crossword puzzles, or horse races

ITR 2 is also the appropriate form when you have received stock options (ESOPs) and the perquisite has been taxed under Section 17(2) of the Income Tax Act.

Practical Example: Priya Mehta is a software architect earning ₹28 lakh from salary. During FY 2025-26, she sold mutual fund units earning ₹4.2 lakh in long-term capital gains and also received ₹1.8 lakh in short-term capital gains from listed shares. Priya must file ITR 2, not ITR 1. Using ITR 1 would render her return defective.

ITR 3: The Right Form for Business Owners & Professionals

Who Needs to File ITR 3 for ITR Filing 2025-26?

ITR-3 is for individuals and HUFs earning income from a proprietary business or as a professional (doctor, lawyer, architect, consultant, etc.) and who are NOT eligible for the presumptive taxation scheme under Section 44AD, 44ADA, or 44AE or who opt out of it.

ITR 3 is mandatory if:

- You carry on a business and your turnover exceeds ₹2 crore (thus ineligible for Section 44AD presumptive scheme)

- You are a professional (covered under Section 44ADA) but your gross receipts exceed ₹75 lakh

- You are a partner in a firm (your share of profit/remuneration from the firm is reported here)

- You opt out of the presumptive scheme after having adopted it in the preceding 5 years

- You have business income as well as capital gains, salary, or other heads of income

ITR 3 requires a detailed Balance Sheet and Profit & Loss Account if your business turnover exceeds specified thresholds. This is where the expertise of a qualified CA becomes indispensable. Dr. Haresh Adwani and the team at Adwani and Company routinely assist business owners in preparing audit-ready financial statements and filing ITR 3 accurately and on time.

ITR 4 (Sugam): Presumptive Taxation & ITR Filing 2025-26 Made Easy

Who Is Eligible for ITR 4?

ITR-4, known as Sugam (meaning “convenient”), is designed for individuals, HUFs, and Partnership Firms (other than LLPs) who opt for the Presumptive Taxation Scheme under Sections 44AD, 44ADA, or 44AE of the Income Tax Act. For ITR filing 2025-26, ITR-4 is available if:

- You are a small business owner with a turnover of up to ₹2 crore and opt for Section 44AD (presuming 8% or 6% net profit)

- You are a specified professional (doctor, lawyer, engineer, architect, accountant, etc.) with gross receipts up to ₹75 lakh and opt for Section 44ADA (presuming 50% as net income)

- You are a goods carriage operator covered under Section 44AE

- Your total income does not exceed ₹50 lakh

- You have income from salary/pension and one house property in addition to presumptive business income

Who Cannot Use ITR 4?

- Individuals who are Directors in a company

- Those who have invested in unlisted equity shares

- Taxpayers with foreign assets or income

- Taxpayers with capital gains from any source

- Individuals with agricultural income exceeding ₹5,000 (unless specifically eligible)

Practical Example: Suresh Patil is a freelance graphic designer based in Pune with gross professional receipts of ₹32 lakh for FY 2025-26. He opts for Section 44ADA presumptive scheme. His total presumptive income is ₹16 lakh (50% of ₹32 lakh). He has no capital gains and no foreign income. Suresh should file ITR-4 for ITR filing 2025-26 it’s simpler, requires no detailed books of accounts, and still keeps him fully tax-compliant.

ITR 1 vs ITR 2 vs ITR 3 vs ITR 4: Quick Comparison for AY 2026-27

| Feature | ITR 1 | ITR 2 | ITR 3 | ITR 4 |

| Salary / Pension | ✔ | ✔ | ✔ | ✔ |

| Capital Gains | ✘ | ✔ | ✔ | ✘ |

| Business Income | ✘ | ✘ | ✔ | Presumptive only |

| Foreign Assets / NRI | ✘ | ✔ | ✔ | ✘ |

| Multiple House Property | ✘ | ✔ | ✔ | ✘ |

| Income Limit | ₹50 L | No limit | No limit | ₹50 L |

| Presumptive Scheme | ✘ | ✘ | ✔ (opt-out) | ✔ |

How to File Your ITR Online for ITR Filing 2025-26: Step-by-Step

The Income Tax Department of India provides a fully online filing platform at incometax.gov.in. Here is a concise step-by-step process:

- Log in to the Income Tax e-filing portal using your PAN and password.

- Navigate to e-File > Income Tax Returns > File Income Tax Return.

- Select Assessment Year 2026-27 and choose the filing mode (Online recommended).

- Select the correct ITR form based on your income profile (use the analysis above).

- Reconcile pre-filled data with your Form 16, Form 26AS, AIS, and TIS.

- Compute your tax liability, claim all eligible deductions and rebates.

- Pay any outstanding tax via Challan 280 (Self-Assessment Tax) before submitting.

- Submit the return and verify it immediately via Aadhaar OTP, Net Banking, or EVC. Without verification, the return is invalid.

Dr. Haresh Adwani emphasizes: “The biggest mistake taxpayers make is treating ITR filing as a one day activity. Accurate ITR filing 2025-26 requires reconciling your salary slips, bank statements, investment proofs, and AIS data at least a week in advance. Rushing leads to errors errors lead to notices.”

Common Mistakes to Avoid During ITR Filing 2025-26

- Selecting ITR 1 despite having capital gains from equity MF redemptions (LTCG/STCG reportable in ITR 2)

- Not reporting exempt income like long-term capital gains on equity up to ₹1.25 lakh it is exempt but must still be disclosed

- Ignoring interest income from savings accounts, FDs, and post office deposits

- Missing foreign asset disclosures in Schedule FA penalties under the Black Money Act can be severe

- Failing to verify the return within 30 days an unverified return is treated as not filed

- Not matching TDS credits with Form 26AS before claiming refunds mismatches delay processing

- Wrong bank account details for refund credit

Frequently Asked Questions (FAQs)

1. What is the due date for ITR filing 2025-26 for individuals?

For individuals not requiring a tax audit, the due date for filing the income tax return for FY 2025-26 (AY 2026-27) is July 31, 2026. For taxpayers liable for audit under Section 44AB, the due date is October 31, 2026. Filing after the due date attracts a late fee under Section 234F of up to ₹5,000.

2. Can I switch between new and old tax regime in ITR filing 2025-26?

Yes. Salaried individuals can switch between the new and old tax regime each year at the time of ITR filing 2025-26. However, taxpayers with business income can opt out of the new regime only once. After opting out, they cannot return to the new regime in future years (with limited exceptions).

3. What is the difference between ITR 3 and ITR 4?

ITR-4 is for taxpayers who opt for the presumptive taxation scheme (Sections 44AD, 44ADA, 44AE) ideal for small businesses and professionals. ITR 3 is for business owners and professionals who maintain full books of accounts, have higher turnover, or opt out of the presumptive scheme. ITR 3 is more comprehensive and may require a tax audit.

4. Is it mandatory to file ITR if income is below the taxable limit?

Filing an ITR is mandatory for certain categories even if income is below the basic exemption limit for example, if TDS has been deducted and you want a refund, if you own foreign assets, or if your electricity consumption or foreign travel expenditure exceeds specified thresholds. Proactive filing also builds a credit history useful for visa applications and loans

5. How can Adwani and Company help with ITR filing 2025-26?

Adwani and Company, led by Dr. Haresh Adwani, offers end-to-end ITR filing services from form selection and Form 26AS reconciliation to computation, filing, and post-filing support for notices and refund follow-ups. Whether you are a salaried individual, business owner, professional, or NRI, the firm handles income tax return 2025-26 with accuracy and confidentiality.

Conclusion:

The choice between ITR 1, ITR 2, ITR 3, and ITR 4 is not merely administrative it is a legal declaration of your income profile to the Government of India. Filing the wrong form can unravel an otherwise accurate return, triggering notices and delays that no taxpayer wants to deal with.

The good news? With a clear understanding of each form’s eligibility criteria and the right guidance from a qualified professional ITR filing 2025-26 can be completed accurately, efficiently, and well ahead of the deadline. The key is to act early: gather your documents, reconcile your AIS, choose the correct form, and file with confidence.

Dr. Haresh Adwani, with his dual expertise in Commerce and Law, has guided thousands of individuals and businesses through the complexities of income tax compliance. His philosophy is simple: “Tax compliance is not a burden it’s a system. Understand the system and it works for you.”.

About the Author

Nidhi Adwani

Nidhi Adwani is the Human Resources Manager at Adwani & Co. She is a Law Graduate and holds an MBA in Human Resources. She manages recruitment, employee engagement, team development, workplace culture, and the firm’s social media and content activities. Passionate about people and organizational growth, she also contributes articles for ITRAdvisor and Adwani & Co. Her writing focuses on HR practices, leadership, workplace engagement, and professional development, offering practical insights for professionals and businesses.

Legal Disclaimer: This article is published for informational and educational purposes only. Nothing contained herein constitutes legal, financial, or tax advice, nor should it be treated as a substitute for professional consultation tailored to your specific circumstances. Tax laws, rates, and provisions are subject to change; readers are strongly advised to consult a qualified Chartered Accountant or tax advisor before acting on any information in this article.

All content is original. References to government portals and statutory provisions are paraphrased for educational purposes in compliance with fair use principles. No content has been reproduced from third-party sources