You did everything right. You filed your Income Tax Return, then realized you missed some income a forgotten freelance payment, some interest from a savings account, maybe rental income you overlooked. So you did the responsible thing: you filed an Updated Return (ITR-U) to correct it.

Then the letter arrived.A Section 143(2) notice after ITR-U. And suddenly that correction you filed feels pointless. This is one of the most misunderstood situations in Indian income tax and it catches thousands of honest taxpayers off guard every year.

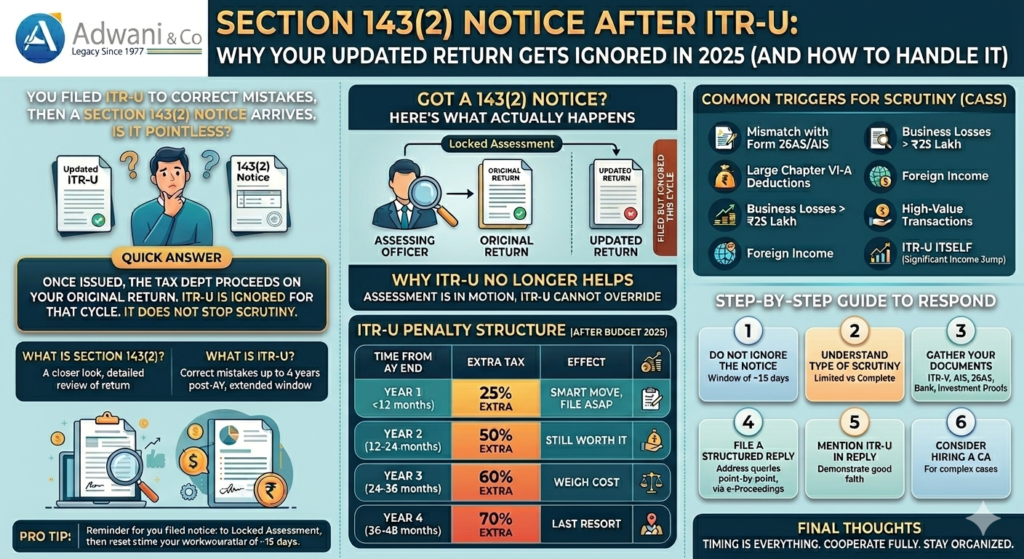

| Quick Answer: Once a Section 143(2) notice after ITR-U is issued, the tax department proceeds on your original return. Your updated return is filed but ignored for that assessment cycle. Filing ITR-U after the notice does NOT stop scrutiny and does NOT update the return being examined. |

What is Section 143(2) Notice After ITR-U?

Understanding Section 143(2) in Simple Terms

Section 143(2) of the Income Tax Act is basically the tax department saying: “We have selected your return for a closer look.” It is a scrutiny notice meaning an Assessing Officer (AO) will review your return in detail to make sure you have not underreported income, overclaimed deductions, or underpaid tax.

This notice must be issued within 3 months from the end of the financial year in which you filed your return. If you filed your ITR on 31st July 2024, the last date for this notice is 30th June 2025.

What is ITR-U (Updated Return)?

ITR-U is a provision under Section 139(8A) that lets you correct a previously filed return or even file one you missed entirely. After Budget 2025, the window to file an ITR-U has been extended from 2 years to 4 years from the end of the relevant Assessment Year. This is a huge change that gives taxpayers much more time to come clean voluntarily.

Got a 143(2) Notice After Filing ITR-U? Here is What Actually Happens

Here is where things go wrong. When you receive a Section 143(2) notice after ITR-U, the assessment is locked onto your original return. The Assessing Officer proceeds on what you originally filed your ITR-U correction is set aside for that cycle. It is not that your ITR-U disappears, it is just that it cannot change the course of the ongoing scrutiny.

This is established under CBDT guidelines and supported by multiple tribunal rulings across India.

Filed ITR-U But Got a 143(2) Notice? Here is Why It No Longer

Helps Think of it this way. Imagine a court case is already running. You cannot suddenly submit new evidence from outside and expect the proceedings to restart from scratch. The same logic applies here.

Once scrutiny proceedings begin under Section 143(3), the assessment is in motion. Your ITR-U filed after a Section 143(2) notice after ITR-U cannot override or pause this process. The law is clear on this the updated return has no bearing on an assessment that is already underway.

A Real-World Example

Arjun, a software engineer in Pune, forgot to report Rs. 3 lakh in freelance income from a foreign client. He filed ITR-U to disclose it. But two weeks before filing ITR-U, he had already received a Section 143(2) notice for the same year.

Result: The AO ignored the ITR-U, conducted scrutiny on the original return, added the Rs. 3 lakh as undisclosed income, and imposed a penalty. Arjun had to cooperate with the scrutiny process his ITR-U counted for nothing in that cycle.

Also Read:

https://www.adwaniandco.com/blog/section-153c-tax-notice-guide

Common Triggers That Cause Section 143(2) Notice After ITR-U

Not every taxpayer gets selected for scrutiny.

The tax department uses a system called CASS (Computer Assisted Scrutiny Selection) to automatically flag cases. Here are the most common reasons your case might be picked:

- Mismatch with Form 26AS or AIS: If the income shown in your ITR does not match what banks, employers, or other sources have reported, the system flags it automatically.

- Large deductions under Chapter VI-A: Claiming very high 80C, 80D, or home loan deductions compared to your income level raises a red flag.

- Business losses above Rs. 25 lakh: Loss claims are always scrutinized more carefully.

- ITR-U itself can trigger scrutiny: Ironically, filing a large update can draw attention. If your ITR-U shows a significant jump in income from the original, it may invite the very notice you were trying to avoid.

- Foreign income or overseas assets: NRIs and those with foreign bank accounts or investments are subject to stricter scrutiny.

- High-value transactions not disclosed: Property sales, large cash deposits, or luxury purchases appearing in your AIS but missing from your ITR.

In the financial year 2024-25 alone, over 1.5 lakh cases were selected for scrutiny a 20% increase from the previous year. With AI-driven audits becoming the norm, this number is only going to grow.

Step-by-Step Guide to Respond to Section 143(2) Notice After ITR-U

Receiving this notice is stressful. But it does not have to be a disaster. Here is exactly what to do, in order:

Step 1: Do Not Ignore the Notice

This is the most critical point. Ignoring a Section 143(2) notice after ITR-U is the worst thing you can do. You have a window typically 15 days to acknowledge the notice through the e-Proceedings portal on the Income Tax website. Log in, go to e-Proceedings, and confirm receipt.

Step 2: Understand What Type of Scrutiny You Are Under

There are two types. Limited scrutiny means the AO can only examine specific issues mentioned in the notice for example, a mismatch in capital gains or TDS credits. Complete scrutiny means your entire return is being reviewed. Knowing which one you are dealing with helps you prepare.

Step 3: Gather Your Documents

- ITR-V (acknowledgement of your original filed return)

- Form 26AS and Annual Information Statement (AIS)

- Bank statements for the full financial year

- Investment proofs for all deductions claimed (80C, 80D, HRA, etc.)

- Details of all income sources including salary slips, rent agreements, freelance invoices

- Copy of your ITR-U filing acknowledgement

Step 4: File a Structured Reply

Your reply must address each query raised in the notice, point by point. Use a professional format with clear headings. Attach supporting documents as PDF scans. All replies must go through the e-Proceedings portal emails or physical visits have no legal value under the faceless assessment system.

Step 5: Mention Your ITR-U in the Reply

Even though your ITR-U does not override the scrutiny, mention it in your submission. State clearly that you had filed an Updated Return to voluntarily disclose additional income this demonstrates good faith and may be considered during penalty determination.

Step 6: Consider Hiring a CA

If your case involves complex income sources, large deductions, or significant additional tax demand, hire a Chartered Accountant. Scrutiny proceedings involve technical legal language and strict deadlines. A CA who handles tax assessments regularly will know exactly what to say, what to submit, and how to protect you.

Step 7: Appeal if the Order is Unfavorable

After the AO passes the final order under Section 143(3), you have 30 days to file an appeal with the Commissioner of Income Tax (Appeals) or CIT(A). If you have cooperated fully and have documented everything properly, your chances of getting relief on appeal are good.

| Pro Tip: Track your case status by logging into incometax.gov.in and checking the e-Proceedings tab. If a Section 143(2) notice after ITR-U has been issued, it will appear here. You will also receive an email and SMS to your registered contact details. |

Three Real Case Studies: What Happened to Taxpayers Like You

Case 1: Salaried Employee Who Cooperated Fully

Rajesh, a 34-year-old engineer from Pune, had forgotten to report a Rs. 2 lakh performance bonus from a previous employer. He filed ITR-U to correct this but had already received a Section 143(2) notice after ITR-U for the same year. His ITR-U was ignored in the scrutiny. However, Rajesh cooperated fully, submitted all documents on time, and mentioned the ITR-U as evidence of good faith. The AO raised a demand of Rs. 50,000. On appeal, Rajesh got relief and the demand was reduced significantly.

Case 2: Small Business Owner Who Caught a Break

Priya ran a small cafe and had claimed excess depreciation on her equipment. She filed ITR-U late. A Section 143(2) notice followed. The AO examined her original return and questioned the depreciation claim. Priya submitted invoices, purchase records, and depreciation schedules. The final demand was reduced by 40% from the initial assessment.

Case 3: Freelancer Who Ignored the Notice A Warning

Vikram, a graphic designer, received a Section 143(2) notice after ITR-U but assumed it would resolve itself. He did not respond. The AO passed a best judgment assessment under Section 144 essentially guessing his income based on available data and raised a demand of nearly double the actual tax due, plus a 200% penalty.

How to Prevent Section 143(2) Notice After ITR-U in the Future

Prevention is always better than a cure. Here is how to reduce the chances of landing in this situation again:

- File accurately the first time: Cross-check your ITR against Form 26AS and the Annual Information Statement (AIS) before submitting. Most mismatches that trigger scrutiny are simple oversights.

- Use ITR-U only before any notice: If you realize a mistake, file ITR-U as soon as possible before any scrutiny notice arrives. The 4-year window gives you plenty of time, but earlier is always better.

- Use the pre-fill option on the e-filing portal: The portal automatically pulls data from your AIS, Form 26AS, and employer records. Using this reduces the chance of missing income.

- Keep all financial documents organized: Rent agreements, investment proofs, bank statements, salary slips keep these ready every year. Scrutiny can happen to any return, anytime.

- Hire a CA for complex cases: If your annual turnover exceeds Rs. 1 crore, you have multiple income sources, or you have foreign assets do not file alone. Professional guidance upfront is far cheaper than fighting a scrutiny assessment later.

1.Can I file ITR-U after receiving a 143(2) notice?

Technically yes you can still file ITR-U after receiving the notice. But it will be ignored for the ongoing scrutiny assessment. The Assessing Officer will proceed on your original return. Your ITR-U may still count as a gesture of good faith during penalty proceedings

2.Does filing ITR-U stop a 143(2) notice?

No. Filing ITR-U has no power to stop, pause, or cancel a Section 143(2) scrutiny notice. Once issued, the notice runs its full course regardless of any ITR-U filed before or after.

3.How long does a scrutiny assessment take?

Typically between 6 months to 1.5 years from the date of the notice. Under the faceless assessment system, the entire process is digital and can move faster than traditional scrutiny.