Why NRI Tax Planning Before Returning to India Matters

Every year, thousands of Non-Resident Indians working in the United States, Canada, United Kingdom, UAE, Australia, and other countries make the decision to return home. For many, it is driven by family, career opportunities, or simply the desire to reconnect with their roots. But what often comes as a surprise sometimes a very expensive one is how dramatically their tax situation changes the moment they step back on Indian soil for good.

According to guidelines issued by the Income Tax Department of India, your residential status determines the scope of your tax liability. As an NRI, you are taxed only on income earned or received in India. The moment your status changes to Resident, however, India gains the right to tax your global income including income from foreign bank accounts, rental earnings from property abroad, dividends from US or UK stocks, and money you earn from global investments.

This is why NRI tax planning before the return journey is not just advisable it is essential. Dr. Haresh Adwani of Adwani & Company has guided hundreds of returning NRIs through this transition, and consistently observes that those who plan ahead save significantly more, comply cleanly, and avoid stressful tax notices later.

Important Alert

Many NRIs believe their foreign income is permanently outside India’s tax net. This is incorrect once you become a tax resident. The planning window particularly your RNOR period is limited and time-sensitive.

NRI Tax Rules: When Do You Become Resident, RNOR, or ROR?

Understanding your residential status is the very first step in NRI tax planning in India. The Income Tax Act, 1961 defines three categories of residential status for individuals:

| Status | What It Means | Indian Tax on Foreign Income? |

|---|---|---|

| NRI (Non-Resident Indian) | Stays less than 182 days in India in a year (general rule) | Not Taxable |

| RNOR (Resident but Not Ordinarily Resident) | Transitional status for returning NRIs; limited foreign tax exposure | Partially Exempt |

| ROR (Resident and Ordinarily Resident) | Full tax resident; all global income taxable in India | Fully Taxable |

The RNOR status is arguably the most valuable tool available to a returning NRI — but it is available only for a limited period, typically two to three financial years after returning, depending on your prior NRI history. During this window, your foreign income remains outside India’s tax net, giving you critical time to restructure investments and repatriate funds in a tax-efficient manner.

Dr. Haresh Adwani strongly advises every returning professional to calculate their RNOR window as the very first step, ideally six to twelve months before the planned return date.

Also Read:

https://www.adwaniandco.com/blog/the-120-day-rule-that-is-silently-taxing-thousands-of-nris-in-india

The 120-Day Rule That Silently Traps NRIs

Here is a less-known but critically important provision in India’s NRI tax rules that catches many people completely off guard. Most NRIs believe that as long as they live outside India, their NRI status is protected. But there is a specific rule, introduced via the Finance Act 2020, that can strip your NRI status even if you live abroad.

If the following three conditions are all true, you may be classified as a tax resident of India even though you live abroad:

The Three-Condition Rule

1. Your income from India exceeds ₹15 lakh in the financial year

2. You stayed in India for 120 days or more in that financial year

3. You stayed in India for 365 days or more cumulatively over the previous four financial years

120 days sounds like a lot. But consider this you come for a wedding in December, stay through January. You visit again in April for a family function. You attend a relative’s medical emergency in August. Without consciously tracking, you may have crossed the 120-day threshold without even realising it. And if your Indian income salary from an Indian employer, rent from property, or dividend from Indian shares exceeds ₹15 lakh, India’s tax jurisdiction now extends to your global income.

This is not a hypothetical risk. At Adwani & Company, we have advised clients who received income tax notices specifically because of this provision. The solution is straightforward track your travel days carefully and consult a qualified NRI tax advisor well before the end of each financial year (March 31).

10 NRI Tax Questions You Cannot Afford to Ignore

Based on years of advising professionals returning from the US, UK, UAE, Canada, Singapore, and Australia, Dr. Haresh Adwani has compiled the ten most important NRI tax questions that arise during the return transition. Each of these has significant financial implications if not addressed in advance.

1. When exactly will I become Resident, RNOR, or ROR in India? Your status depends on your physical presence over multiple financial years. Calculating this accurately determines your tax liability strategy.

2. If I sell my US or UK stocks after returning, where will the capital gains be taxed? Gains on foreign stocks can be taxed in both India and the country where the assets are held, unless DTAA provisions apply. Selling while still RNOR can make a significant difference.

3. How can I avoid double taxation between India and my country of work? India has Double Taxation Avoidance Agreements (DTAA) with over 90 countries. Understanding which provisions apply to your income type is crucial.

4. Can I claim Foreign Tax Credit (FTC) in India for taxes already paid abroad? Yes, under Rule 128 of the Income Tax Rules, you can claim credit for foreign taxes paid. However, the process requires Form 67 and specific documentation.

5. What happens to my foreign bank accounts and investments once I become a resident? Your NRE and FCNR accounts must be re-designated to RFC (Resident Foreign Currency) accounts. Failure to do so is a FEMA violation with serious penalties.

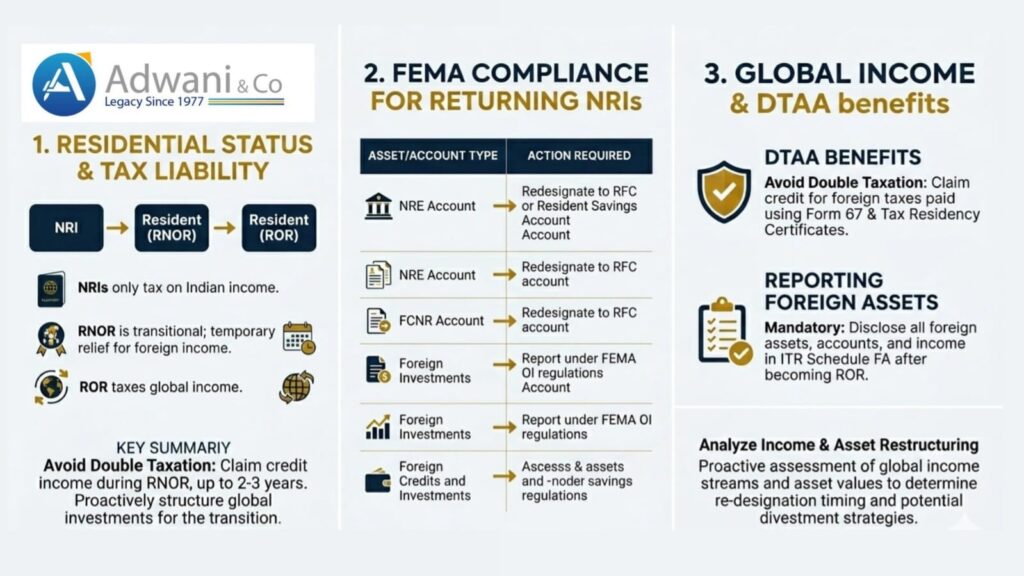

6. Do I need to report foreign assets in my Indian income tax return? Absolutely. Once you become a full Resident (ROR), you must disclose all foreign assets, accounts, and income in Schedule FA of your ITR. Non-disclosure attracts severe penalties under the Black Money Act.

7. Should I sell some investments while I am still RNOR rather than waiting until ROR? In many cases, yes. Since foreign income is not taxable during the RNOR period, strategic divestment of foreign assets during this window can produce significant tax savings.

8. How are RSUs, ESOPs, and stock compensation from foreign employers taxed in India? This is complex. RSUs may be taxed both when they vest (as salary income) and when sold (as capital gains). DTAA provisions and the nature of your resident status at both events determine the outcome.

9. What are the tax implications if I sell property in India after returning? The tax treatment depends on the holding period, whether you are RNOR or ROR at time of sale, and available exemptions under Section 54 or 54EC of the Income Tax Act.

10. How can I bring my foreign savings to India in a legal and efficient way? FEMA governs the repatriation of foreign funds. The RFC account and LRS (Liberalised Remittance Scheme) framework provides structured pathways to bring money in compliantly.

Real-World Example: IT Professional Returning from the US

Rajesh S., Software Engineer San Francisco to Pune

Rajesh worked in the US for 14 years on an H-1B visa and decided to return to India in July 2025. He had accumulated USD 280,000 in a US brokerage account (mostly tech stocks with significant unrealised gains), USD 95,000 in a 401(k) retirement account, and owned a property in Pune generating ₹18 lakh annual rent.

Without Planning: Had Rajesh returned and immediately converted his NRE account, sold his US stocks after becoming ROR, he would have faced Indian capital gains tax on the full appreciation potentially ₹40–50 lakh in additional tax liability, plus mandatory disclosure of all foreign assets.

With Planning via Adwani & Company: By calculating his RNOR window (approximately 2 financial years), Rajesh sold his US stocks strategically during that period when foreign income was not taxable in India. His NRE and FCNR accounts were re-designated to RFC accounts in time. Form 67 was filed correctly to claim US tax credit. Penalty exposure was eliminated entirely.

FEMA Compliance for Returning NRIs: What You Must Do

The Foreign Exchange Management Act (FEMA) governs how Indian residents including returning NRIs manage their foreign currency assets, bank accounts, and international transactions. Violations under FEMA are taken seriously by the Enforcement Directorate and can attract penalties many times the value of the transaction involved.

As per Reserve Bank of India (RBI) guidelines, the following changes must be made immediately upon returning to India as a resident:

| Account/Asset Type | Action Required | Deadline |

|---|---|---|

| NRE (Non-Resident External) Account | Re-designate to RFC or Resident Savings Account | Immediately upon change of status |

| FCNR (Foreign Currency NR) Account | Re-designate to RFC account | At maturity or immediately |

| NRO (Non-Resident Ordinary) Account | Re-designate to ordinary resident savings account | Immediately upon change of status |

| Foreign Bank Accounts | Declare in ITR Schedule FA; permitted to retain under FEMA | Annual ITR filing deadline |

| Foreign Investments | Declare and report under FEMA OI regulations | Annual reporting cycle |

Dr. Haresh Adwani advises every returning NRI to consult an authorised FEMA practitioner as a first step not after they have returned, but three to six months before the anticipated return date. This provides time to restructure accounts, repatriate funds, and file necessary declarations without rushing.

Learn more about our NRI FEMA Compliance Services at Adwani & Company.

Pre-Return NRI Tax Planning Checklist

If you are planning to return to India within the next six to eighteen months, use this checklist to ensure you enter the transition fully prepared:

- Calculate your RNOR eligibility window based on your exact NRI years — this is your most valuable planning asset

- Identify all foreign assets: stocks, mutual funds, retirement accounts (401k, IRA, pension), bank accounts, and property

- Evaluate which assets to sell before returning versus during the RNOR window versus after becoming ROR

- Check whether DTAA provisions between India and your country of residence apply to your income types

- Arrange re-designation of NRE, FCNR, and NRO accounts to RFC before or immediately upon return

- Obtain Form 67 documentation for claiming Foreign Tax Credit on income taxed abroad

- Ensure your ITR includes Schedule FA for all foreign assets once you attain ROR status

- Consult a qualified NRI tax advisor ideally one registered with ICAI and experienced in international tax

Read our detailed guide on NRI Taxation and FEMA Compliance — A Complete Handbook for deeper coverage of each checklist item.

DTAA Benefits: How Returning NRIs Can Avoid Double Taxation

One of the most powerful tools available to a returning NRI is the Double Taxation Avoidance Agreement (DTAA). India has signed DTAAs with over 90 countries including the United States, United Kingdom, UAE, Canada, Australia, Singapore, and Germany. These agreements ensure that the same income is not taxed twice once in the country where it is earned and again in India.

However, DTAA benefits are not automatic. You must actively claim them, file the correct forms, and provide the necessary documentation including Tax Residency Certificates (TRC) and Form 10F. The specific provisions vary significantly by country and income type. For instance, the India-US DTAA has specific provisions for employment income, dividends, and capital gains each with different conditions and rates.

ℹ DTAA Quick Tip

For NRIs returning from the UAE, note that the India-UAE DTAA was renegotiated and updated. The provisions affecting salary income and capital gains have changed. Ensure you are referencing the most current treaty text, or consult Adwani & Company for up-to-date guidance specific to your income profile.

Conclusion: Your Return to India Deserves a Well-Crafted Tax Strategy

Returning to India after years abroad is an emotionally significant and practically complex decision. The financial implications spanning NRI tax rules, RNOR status planning, FEMA compliance, DTAA benefits, and foreign asset disclosure require careful attention and expert guidance well before the moving date.

The good news is that with proper NRI tax planning, the transition can be managed smoothly. The RNOR window is a legitimate and powerful tool. DTAA provisions can significantly reduce your tax burden. FEMA compliance, when handled proactively, is straightforward. The 120-day rule, once you are aware of it, is entirely manageable.

The critical factor is timing. Tax planning done before the return preserves options. Tax planning attempted after the return or worse, after a notice from the Income Tax Department is reactive, expensive, and stressful. As Dr. Haresh Adwani consistently advises clients: the best time to plan your return tax strategy is at least six to twelve months before you board that flight home.

Frequently Asked Questions:

1. What is RNOR statusand how does it benifit a returning NRI?

RNOR stands for Resident but Not Ordinarily Resident. It is a transitional tax status available to returning NRIs for a limited period typically two to three financial years after returning, depending on the number of years they were NRI. During the RNOR period, India does not tax income that is earned outside India and not received in India. This makes the RNOR window a critical opportunity to restructure foreign investments and repatriate funds tax-efficiently. Calculating your exact RNOR window is the most important first step in any returning NRI tax planning exercise.

2. Do i need to report my foreign bank accounts after returning to india?

Yes. Once you attain ROR (Resident and Ordinarily Resident) status, you are required to disclose all foreign bank accounts, financial assets, and income from foreign sources in Schedule FA (Foreign Assets) of your Income Tax Return. Non-disclosure is treated as a violation under the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015, which prescribes severe penalties including a flat 30% tax plus a 90% penalty on undisclosed amounts. Proactive disclosure and professional guidance from a qualified NRI tax advisor is strongly recommended.

3. How are RSUs and ESOPs from a US employer taxed when i return to india?

RSUs (Restricted Stock Units) and ESOPs (Employee Stock Option Plans) granted by foreign employers are taxed at two points first at vesting (treated as perquisite or salary income) and again at sale (capital gains). If you are RNOR when the shares vest, there may be no Indian tax at vesting for foreign-source income. However, gains on sale after becoming ROR are fully taxable in India. The India-US DTAA may provide relief on employment income. Given the complexity, consulting a specialist NRI tax advisor who handles cross-border equity compensation is highly advisable.

4. can keep my NRE account after returning to india?

No. Under FEMA regulations, once your residential status changes to Resident Indian, your NRE (Non-Resident External) account must be re-designated to a Resident Foreign Currency (RFC) account or a regular resident savings account. Continuing to operate an NRE account after becoming a resident is a FEMA violation and can attract penalties under the Enforcement Directorate. The re-designation must happen promptly upon change in status. Similarly, FCNR accounts must be re-designated to RFC accounts at maturity.

5.Is the 120-day rule applicable to all NRIs only thoes with high indian income?

The 120-day rule applies specifically to NRIs whose Indian income exceeds ₹15 lakh in the relevant financial year. If your Indian income is below this threshold, the standard 182-day rule applies for determining NRI status. However, if your Indian income from sources such as rent, salary from Indian companies, or interest from NRO accounts exceeds ₹15 lakh, then staying 120 days or more in India in a financial year, combined with a cumulative stay of 365 days in the previous four years, can make you a resident for tax purposes. Tracking your India travel days carefully is essential if you have significant Indian income.

6.what is best time to sell foreign stock-before returning or after returning

The timing of foreign asset liquidation is one of the highest-impact NRI tax planning decisions. Selling before returning (when you are still an NRI) means the gains are taxed only in the country where the asset is held not India. Selling during the RNOR window means the gains from foreign sources are not taxable in India under current provisions. Selling after becoming ROR means full Indian capital gains tax applies. The optimal strategy depends on the specific country, the type of asset, applicable DTAA provisions, and your income profile. Dr. Haresh Adwani and the team at Adwani & Company specialise in creating personalised divestment plans for returning NRIs.

7. How do i claim Foreign Tax Credit(FTC) in india?

Foreign Tax Credit in India is governed by Rule 128 of the Income Tax Rules, 1962. To claim FTC, you must file Form 67 on the income tax e-filing portal before the due date of your return. You will need documentation including a tax payment certificate or withholding statement from the foreign country confirming the taxes paid. The credit is available against the Indian tax payable on the same income, up to the Indian tax liability on that income. FTC cannot create a refund it can only reduce your Indian tax to zero on the relevant income. Missing the Form 67 deadline means losing the credit entirely.

Author

CA. Manish R. Mata Practising In India (Ex – PwC), At Adwani & Co LLP leads the International Accounting & Tax Support vertical, delivering structured execution assistance to US CPA firms and overseas businesses.