ESOP Taxation India

My company has granted me ESOPs worth ₹50 lakh,” a senior employee told me proudly, not long ago. My first question back was simple: “₹50 lakh according to whom?” There was silence. That silence is exactly why understanding ESOP taxation India rules matters so much before you exercise a single option.

Most employees focus only on the headline number printed on their ESOP grant letter. Very few stop to ask when tax actually becomes payable, how the value is calculated, what the Fair Market Value (FMV) really means, or how a tax bill can arrive long before any cash from selling shares does. This guide breaks down ESOP taxation India rules in plain language so you can plan ahead instead of being caught off guard.

What Is ESOP Taxation in India?

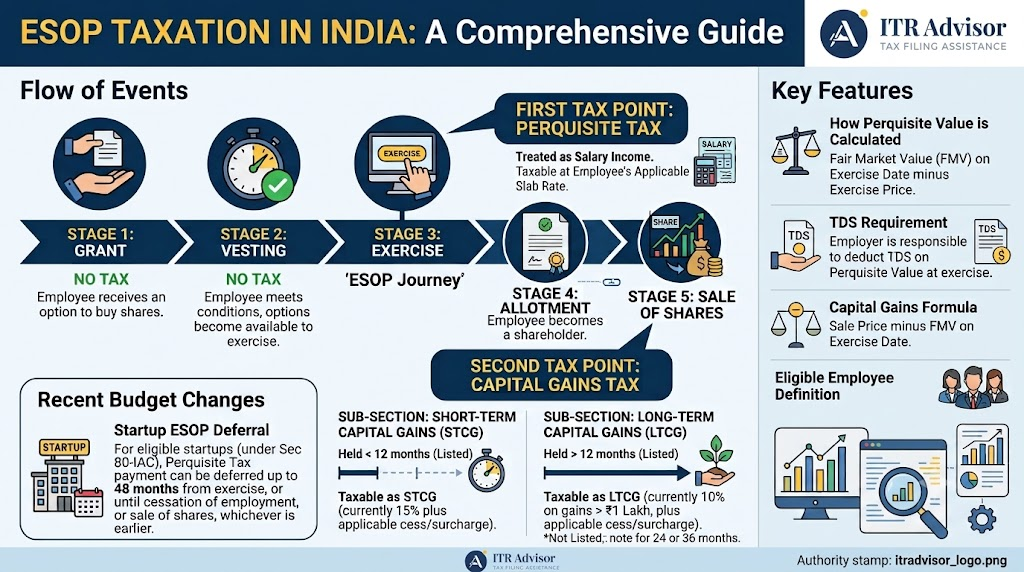

An Employee Stock Option Plan (ESOP) gives you the right to buy company shares at a fixed price, known as the exercise price, after a vesting period. Under ESOP taxation India rules, tax is not a single event it happens in two separate stages, and understanding both is essential to avoid an unpleasant surprise.

Quick Definition ESOP taxation India has two stages: (1) tax as a perquisite (salary income) at the time of exercise, and (2) capital gains tax at the time of eventual sale of shares.

Understanding Fair Market Value (FMV) in ESOP Taxation India

The single most misunderstood concept in ESOP taxation India is the Fair Market Value, or FMV. FMV is not the price you paid (the exercise price); it is the value of the share on the date of exercise, determined through a valuation exercise. For listed companies, FMV is typically the average market price on the stock exchange. For unlisted companies, FMV must be certified by a Category I Merchant Banker, in line with valuation norms referenced by the Income Tax Department under Rule 3(8) of the Income Tax Rules.

The difference between FMV and your exercise price is what gets taxed first — and it is taxed as salary income, irrespective of whether you have sold a single share.

Real Example: ESOP Taxation India in Numbers

Let’s walk through a simple, real-world example of ESOP taxation India in action:

Example Calculation

Exercise Price = ₹100 per share

FMV on date of exercise = ₹600 per share

Number of shares = 10,000 Taxable perquisite = (₹600 – ₹100) × 10,000 = ₹50,00,000

This ₹50 lakh difference is added to your salary income and taxed at your applicable slab rate in the year of exercise — even though you have not received a rupee in cash. This is the core trap that catches employees off guard under ESOP taxation India rules.

ESOP Taxation India: The Two Stages Explained

Stage 1: Perquisite Tax at Exercise

As shown above, the difference between FMV and exercise price is taxed as a perquisite under the head “Salary” in the year you exercise your options. Your employer is required to deduct TDS on this amount, which can significantly reduce your take-home pay in that month.

Stage 2: Capital Gains Tax at Sale

When you eventually sell the shares, the difference between the sale price and the FMV (which now becomes your cost of acquisition) is taxed as capital gains. Depending on the holding period and whether the shares are listed, this may attract short-term or long-term capital gains tax, as outlined under provisions tracked by the Central Board of Direct Taxes. This is the second layer that many employees forget to plan for under ESOP taxation India rules.

Key Questions to Ask Before Exercising ESOPs

Before exercising your options, run through these questions — they form the backbone of sound ESOP taxation India planning:

- What is the latest certified FMV of the shares?

- What will my total tax liability be in the year of exercise?

- Is this the right financial year to exercise, given my other income?

- How was the valuation determined, and by whom?

- What happens if the company is not yet listed and shares are illiquid?

- Will TDS deducted by my employer cover my full liability, or will I owe additional tax?

Common Mistakes in ESOP Taxation India Planning

In our advisory practice, we repeatedly see the same gaps in ESOP taxation India planning:

- Treating the grant letter value as the actual taxable amount.

- Exercising options without checking the current FMV first.

- Ignoring the liquidity problem in unlisted or pre-IPO companies, where tax is due even though shares cannot easily be sold.

- Failing to plan for advance tax obligations arising from a large perquisite in a single year.

- Not maintaining proper documentation of exercise dates, FMV certificates, and TDS, which can later trigger scrutiny.

Read our detailed guide on ESOP Valuation India: What Founders Must Know

How Adwani and Company Supports ESOP Taxation India Planning

Dr. Haresh Adwani, founding partner of Adwani and Company, holds a PhD in Commerce and is also a law graduate, bringing a rare combination of taxation expertise and legal grounding to complex employee compensation matters. This dual qualification is particularly valuable in ESOP taxation India cases, where valuation rules, perquisite computation, and capital gains provisions intersect with company law and FEMA considerations for employees of foreign parent entities.

Under the guidance of Dr. Haresh Adwani, Adwani and Company has helped senior executives and startup employees across Pune and beyond model their exercise-year tax liability in advance, time their option exercise around income peaks and troughs, and stay compliant with documentation expected by the Income Tax Department. The firm’s approach is to look at ESOP taxation India not as a one-time calculation, but as part of a broader personal tax strategy.

Key Takeaways

- ESOP taxation India involves two separate tax events: perquisite tax at exercise and capital gains tax at sale.

- The taxable amount is based on FMV, not the exercise price or the grant letter value.

- Tax can be payable even before you receive any cash from selling shares.

- Unlisted company ESOPs need extra caution due to valuation and liquidity issues.

- Professional guidance from an experienced CA firm like Adwani and Company can prevent costly timing mistakes.

Frequently Asked Questions on ESOP Taxation India

1.How is ESOP taxed in India?

ESOP taxation India works in two stages: a perquisite tax on the FMV-minus-exercise-price difference at exercise, then capital gains tax on the FMV-to-sale-price difference at sale.

2.Is tax payable on ESOPs even before selling the shares?

Yes. The perquisite tax becomes payable in the year of exercise itself, regardless of whether the shares are later sold.

3.How is FMV determined for unlisted company ESOPs?

For unlisted companies, FMV must be certified by a registered Category I Merchant Banker as per Income Tax Rules.

4.What happens if I exercise ESOPs but the company never gets listed?

You may still owe perquisite tax based on the certified FMV, even though the shares remain illiquid, making advance planning essential.

Can Adwani and Company help plan ESOP exercise timing?

Yes, Adwani and Company, under Dr. Haresh Adwani, helps employees project their exercise-year liability and choose an optimal exercise timeline.

Conclusion: Don’t Let ESOP Taxation India Rules Catch You Off Guard

A well-planned ESOP strategy can genuinely create long-term wealth. A poorly planned one can create an unexpected, and sometimes painful, tax bill and most employees only discover this after the damage is done. Understanding ESOP taxation India rules before you exercise, not after, is the single biggest factor separating a smooth outcome from a stressful one.

If you are holding ESOPs and are unsure about the tax impact before exercising, connect with Adwani and Company today. Dr. Haresh Adwani and the team can help you model your liability, time your exercise, and stay fully compliant with applicable tax and regulatory norms tracked by authorities such as the Ministry of Corporate Affairs.

About the Author

Nidhi Adwani is the Human Resources Manager at Adwani & Co. She is a Law Graduate and holds an MBA in Human Resources. She manages recruitment, employee engagement, team development, workplace culture, and the firm’s social media and content activities. Passionate about people and organizational growth, she also contributes articles for ITRAdvisor and Adwani & Co. Her writing focuses on HR practices, leadership, workplace engagement, and professional development, offering practical insights for professionals and businesses.

Legal Disclaimer: This article is published for informational and educational purposes only. Nothing contained herein constitutes legal, financial, or tax advice, nor should it be treated as a substitute for professional consultation tailored to your specific circumstances. Tax laws, rates, and provisions are subject to change; readers are strongly advised to consult a qualified Chartered Accountant or tax advisor before acting on any information in this article.

All content is original. References to government portals and statutory provisions are paraphrased for educational purposes in compliance with fair use principles. No content has been reproduced from third-party sources