Are You Paying More Capital Gains Tax Than You Should?

You just sold a property. Or perhaps you exited mutual funds after years of patient holding. The money lands in your account and instantly the question follows: how much of this belongs to the government?

Capital gains tax in India 2025 is one of the most misunderstood areas of personal finance. Thousands of taxpayers overpay every single year, simply because they do not know the updated rules. Others face compliance notices because they assumed rates from two years ago still apply. The truth is, the Union Budget 2024 fundamentally overhauled the entire capital gains framework, and if you have not updated your knowledge, you are either leaving money on the table or under-reporting tax.

This guide by the experts at Adwani and Company breaks down everything you need to know about capital gains tax in India 2025: the updated rates, revised holding periods, available exemptions, and legal strategies to reduce your tax outgo. Whether you own stocks, real estate, gold, or mutual funds, read this before your next transaction. And if you have already filed or are preparing to file, also read our companion blog: ITR Filing 2026: No Longer Optional at www.adwaniandco.com/blog/itr-filing-2026-no-longer-optional.

What Is Capital Gains Tax in India 2025?

Capital gains tax is the tax levied on the profit you earn when you sell a capital asset. A capital asset includes land, buildings, listed shares, equity mutual funds, debt funds, gold, bonds, debentures, and even intellectual property such as patents and trademarks. When you sell any of these at a profit, the resulting gain is taxable in the financial year of transfer, regardless of when you actually receive the cash.

The Income Tax Department of India classifies capital gains into two broad categories based on how long you held the asset before selling:

- Short-Term Capital Gains (STCG): Profits earned from assets sold before completing the qualifying minimum holding period.

- Long-Term Capital Gains (LTCG): Profits from assets held beyond the qualifying period, attracting lower, preferential tax rates designed to encourage long-term investment.

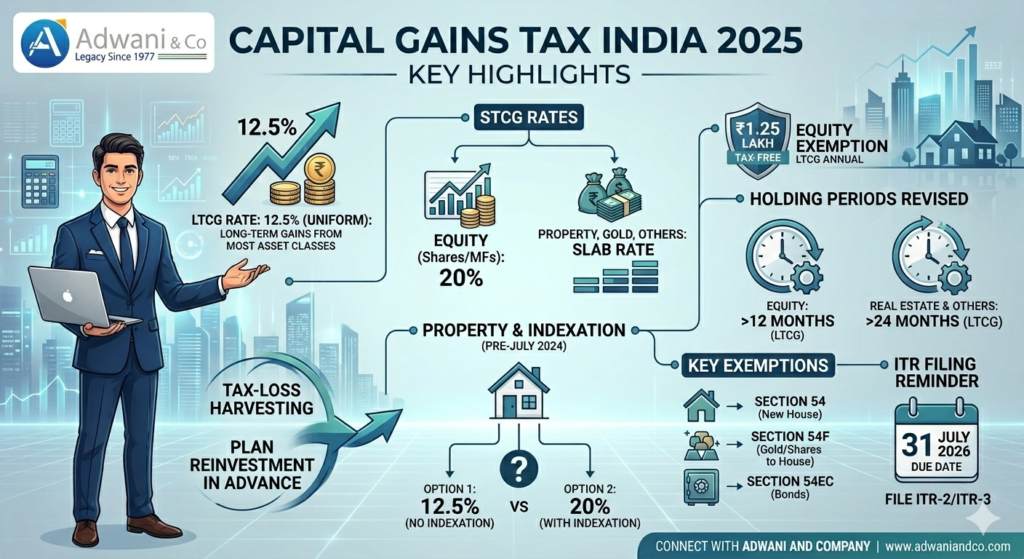

The most important change of the last two years: all LTCG is now uniformly taxed at 12.5% for most asset classes. This replaced a fragmented, asset-specific structure and marks the most significant simplification of capital gains tax in India in decades.

Key Takeaway: Capital gains tax in India 2025 is now simpler structurally but demands sharper planning. The rate is uniform. The strategy is personal.

LTCG vs STCG: Know Your Holding Periods for Capital Gains Tax India 2025

Getting the holding period right is the single most important first step in capital gains tax planning India 2025. Misclassifying a long-term gain as short-term or vice versa leads to either excess tax payment or a compliance notice.

For Listed Equity Shares and Equity-Oriented Mutual Funds:

- Hold for more than 12 months → Long-Term Capital Gain (LTCG) taxed at 12.5% under Section 112A

- Sell within 12 months → Short-Term Capital Gain (STCG) taxed at 20% under Section 111A (revised from 15% effective 23 July 2024)

For Real Estate, Gold, Unlisted Securities, Debt Funds, and Other Assets:

- Hold for more than 24 months → Long-Term Capital Gain (LTCG) at 12.5%

- Sell within 24 months → Short-Term Capital Gain (STCG) taxed at your applicable income slab rate

These rules, effective from 23 July 2024, now apply consistently. As clarified by the Income Tax Department, capital gains are always taxed at special rates outside the regular slab structure, under both the old and new tax regimes.

Equity investor note: The first ₹1.25 lakh of LTCG from listed equity shares and equity-oriented mutual funds remains tax-free each financial year under Section 112A. Only gains above this threshold attract the 12.5% LTCG rate.

Capital Gains Tax Rates India 2025 Complete Rate Table

| Asset Type | Holding Period | Classification | Tax Rate |

| Listed equity shares / equity mutual funds | > 12 months | LTCG (Sec 112A) | 12.5% (₹1.25 lakh exempt) |

| Listed equity shares / equity mutual funds | ≤ 12 months | STCG (Sec 111A) | 20% |

| Real estate, gold, unlisted shares | > 24 months | LTCG | 12.5% (no indexation) |

| Residential property (bought before 23 Jul 2024) | > 24 months | LTCG (choice) | 12.5% without indexation OR 20% with indexation |

| Real estate, gold, other assets | ≤ 24 months | STCG | Income slab rate |

| Debt mutual funds (≤35% equity, bought after 1 Apr 2023) | Any | Special (Sec 50AA) | Income slab rate |

Practical Capital Gains Tax Example India 2025

Example 1: Selling Listed Equity Shares (LTCG with ₹1.25 Lakh Exemption)

Priya bought 2,000 shares of a listed company in May 2024 at ₹150 each. Total cost: ₹3,00,000. She sold all of them in August 2025 at ₹280 each. Sale value: ₹5,60,000.

| Step | Calculation | Amount |

| Holding Period | May 2024 to August 2025 = 15 months | > 12 months → LTCG |

| Total Capital Gain | ₹5,60,000 − ₹3,00,000 | ₹2,60,000 |

| Section 112A Exemption | First ₹1,25,000 is tax-free | −₹1,25,000 |

| Taxable LTCG | ₹2,60,000 − ₹1,25,000 | ₹1,35,000 |

| LTCG Tax @ 12.5% | ₹1,35,000 × 12.5% | ₹16,875 |

| If sold within 12 months (STCG) | ₹2,60,000 × 20% | ₹52,000 (3x higher!) |

This single comparison illustrates why holding equity beyond 12 months is one of the most powerful capital gains tax planning strategies in India 2025.

Example 2: Property Sale Indexation vs No-Indexation Decision

Ramesh purchased a residential flat in Mumbai in April 2012 for ₹45 lakh. He sold it in March 2026 for ₹1.85 crore. Since this property was purchased before 23 July 2024, Ramesh can choose between two tax routes:

| Option | Calculation | Tax Payable |

| 12.5% LTCG (No Indexation) | Gain = ₹1,85,00,000 − ₹45,00,000 = ₹1,40,00,000 × 12.5% | ₹17,50,000 |

| 20% LTCG (With Indexation) | Indexed cost = ₹45L × (376/200) = ₹84.6L; Gain = ₹1,85L − ₹84.6L = ₹1,00.4L × 20% | ₹20,08,000 |

| Best Option | 12.5% without indexation saves ₹2,58,000 in this case | Choose 12.5% |

CII for FY 2025-26 is 376 as notified by CBDT. CII for FY 2012-13 was 200. Always run both calculations before executing a pre-July 2024 property sale. The arithmetic varies with original purchase year and price. Adwani and Company calculates both scenarios for every property client before the transaction date.

Capital Gains Tax Exemptions India 2025 Sections 54, 54F, 54EC

The Income Tax Act offers powerful reinvestment-based exemptions that remain fully intact under the 2024 revised framework. These are your most potent legal tools to reduce or eliminate capital gains tax on property India 2025 and other assets.

Section 54 Reinvestment in Residential Property

If you sell a residential house and reinvest the capital gain (not the full sale proceeds) into another residential house within 1 year before or 2 years after the sale (or construct within 3 years), the gain is fully or partially exempt. Cap: ₹10 crore per financial year from AY 2024-25. Source: Section 54, Income Tax Act, 1961 as amended.

Section 54F Sale of Non-Residential Assets into a House

When you sell any long-term capital asset other than a residential property (gold, shares, commercial property), you can claim exemption by reinvesting the entire sale proceeds (not just the gain) into a new residential house within the specified window. Cap: ₹10 crore from AY 2024-25.

Section 54EC Capital Gains Bonds

Invest up to ₹50 lakh of capital gains in specified government-backed bonds (NHAI, REC) within 6 months of the sale date to claim exemption. These bonds have a lock-in of 5 years.

Capital Gains Account Scheme (CGAS)

If you cannot reinvest before filing your ITR (due date: 31 July 2026 for individuals for FY 2025-26), deposit the gains in a CGAS account at a scheduled bank before the due date. The amount retains its exemption eligibility and must be reinvested within the prescribed period.

Important: These exemptions require advance planning before the transaction not after. Timing the reinvestment correctly is where expert guidance is most valuable.

Indexation and Capital Gains Tax India 2025 What Changed?

Indexation was the most valuable shield for real estate investors. It allowed you to inflate your original purchase cost using the Cost Inflation Index (CII), dramatically reducing taxable gains on long-held property.

- For assets purchased on or after 23 July 2024: Indexation is no longer available. The 12.5% LTCG rate applies without adjustment.

- For residential property purchased before 23 July 2024: Taxpayers retain the option to choose between 12.5% without indexation OR 20% with indexation whichever results in lower tax.

- CII for FY 2025-26: 376 (as notified by CBDT, cbdt.gov.in).

For properties purchased 10–20 years ago at low prices, indexation can still produce a significantly lower tax bill. The math must be done property by property. Adwani and Company runs this calculation for every real estate client.

Capital Gains Tax on Property India 2025 Special Rules

Segregation of Gains by Date

ITR forms now require you to report capital gains separately for transactions completed before and after 23 July 2024, reflecting the two different rate regimes. This is a mandatory compliance requirement for FY 2025-26.

NRI Property Sellers

NRIs selling property in India are subject to TDS deduction at source by the buyer. Advance planning and a Form 13 application to the Income Tax Department can significantly reduce withholding amounts. NRIs selling unlisted shares can also adjust sale consideration for currency fluctuation.

Section 87A Rebate Does NOT Apply to Special Rate Income

Even if your total income is below ₹12 lakh, the Section 87A rebate cannot be claimed against capital gains taxed at special rates (12.5% or 20%). This catches thousands of first-time filers off guard every year.

Share Buybacks Now Taxed as Dividend

From 1 October 2024, proceeds from listed company buybacks are taxed as dividend income in the shareholder’s hands, not as capital gains. The buy cost becomes a capital loss that can be carried forward for up to 8 years.

How to Save Capital Gains Tax Legally Strategies for India 2025

Capital gains tax planning in India 2025 is about using provisions that Parliament has enacted to encourage long-term investment. Here are the most effective legal strategies:

1. Tax-Loss Harvesting Before Year-End

Short-term capital losses can offset both STCG and LTCG. Long-term capital losses can only offset LTCG. Review your portfolio before 31 March each year and book losses strategically to reduce your net taxable gain.

2. Harvest the ₹1.25 Lakh Annual LTCG Exemption Every Year

Every financial year, book up to ₹1.25 lakh of equity LTCG tax-free, then repurchase the same securities to reset your cost basis. Over 10–15 years of consistent application, this strategy alone can save several lakhs in capital gains tax.

3. Stagger Large Sales Across Two Financial Years

If you hold a substantial position, selling across two financial years effectively doubles your annual exemption threshold and keeps gains in lower brackets.

4. Choose the Right Route for Pre-July 2024 Property

Always compute both the indexation and non-indexation options before signing a property sale agreement. The saving can be significant and cannot be reversed after the transaction.

5. Reinvest Under Section 54 / 54F / 54EC in Advance

Identify your reinvestment target before executing the sale, not after. The time windows are strict and missing them forfeits the exemption entirely.

Want expert guidance on capital gains tax planning India 2025? Connect with Adwani and Company today. Visit www.adwaniandco.com or speak to our team for a personalised tax-saving plan.

Capital Gains Tax Filing ITR Forms and Compliance FY 2025-26

Capital gains must be reported in Schedule CG of your Income Tax Return, with the total auto-populating into Part B. For FY 2025-26 (AY 2026-27), here is what applies:

- ITR-1 and ITR-4: Can now report LTCG on equity up to ₹1.25 lakh.

- ITR-2: Required for taxpayers with LTCG from other assets or STCG from any asset.

- ITR-3: Required if you have business income alongside capital gains.

The ITR filing last date for non-audit individuals for FY 2025-26 is 31 July 2026. Missing this deadline triggers interest under Section 234A at 1% per month on unpaid tax, plus a late filing fee of up to ₹5,000 under Section 234F.

Also read: ITR Filing 2026: No Longer Optional Adwani and Company

Trusted Government Sources:

- Income Tax Department e-filing portal: www.incometax.gov.in

- CBDT Circulars and Notifications: www.incometax.gov.in/iec/foportal/help/information/cbdt-notifications

Conclusion: Take Control of Your Capital Gains Tax in 2025

Capital gains tax in India 2025 is structurally simpler than before but strategically more demanding. The uniform 12.5% LTCG rate, revised STCG rates, removal of indexation for new assets, capped Section 54 exemptions, and the new ITR reporting requirements all mean that decisions taken at the point of transaction not after determine your tax bill.

The difference between a well-planned asset sale and a reactive one can easily run into lakhs of rupees. Whether you are a long-term equity investor, a property owner evaluating a sale, or a business owner with diverse assets, structured capital gains tax planning India 2025 is not optional it is financial self-defence.

Frequently Asked Questions Capital Gains Tax India 2025

Q1. What is the capital gains tax rate in India for 2025?

For long-term capital gains (LTCG), the uniform rate is 12.5% for most assets effective from 23 July 2024. For listed equity LTCG above ₹1.25 lakh per year, the rate is 12.5% under Section 112A. Short-term capital gains (STCG) on listed equity is taxed at 20% under Section 111A. STCG on all other assets is taxed at your income slab rate. The new Income Tax Act 2025 does not change these rates but uses revised section numbers from April 2026.

Q2. How much capital gain is tax-free in India in 2025?

LTCG up to ₹1.25 lakh per financial year from listed equity shares and equity-oriented mutual funds is fully exempt under Section 112A. For other capital assets (real estate, gold, debt funds), there is no annual exemption, but reinvestment-based exemptions under Sections 54, 54F, and 54EC can significantly reduce or eliminate the tax liability.

Q3. How to avoid capital gains tax on property sale in India 2025?

You cannot avoid capital gains tax legally, but you can reduce it significantly through: (1) Reinvesting gains in a new residential property under Section 54 or 54F; (2) Investing up to ₹50 lakh in NHAI/REC bonds under Section 54EC within 6 months of sale; (3) For pre-July 2024 properties, choosing the indexation option if it results in lower tax; (4) Parking gains in a Capital Gains Account Scheme (CGAS) before the ITR deadline to preserve exemption eligibility.

Q4. Is indexation still available for property in India 2025?

Indexation is available only for residential property purchased before 23 July 2024. For such properties, taxpayers can choose between 12.5% LTCG without indexation or 20% LTCG with indexation. Always compute both before selling. For property purchased on or after 23 July 2024, only the 12.5% rate without indexation applies.

Q5. Can capital loss be set off against salary income in India?

No. Capital losses can only be set off against capital gains, not against salary or other income. Short-term capital loss (STCL) can offset both STCG and LTCG. Long-term capital loss (LTCL) can only offset LTCG. Unabsorbed losses can be carried forward for up to 8 assessment years, but only if the ITR is filed on time.

Q6. Does Section 87A rebate apply to capital gains tax on shares in 2025?

No. The Section 87A rebate does not apply to capital gains taxed at special rates, whether at 12.5% (LTCG) or 20% (STCG). Even if your total income is below ₹12 lakh, you must pay capital gains tax on these amounts in full. This is one of the most common surprises for first-time filers.

Author

CA Dipesh Gurubakshani is a Chartered Accountant with Adwani & Co LLP, Pune, specialising in income tax audit, direct taxation, and accounting advisory. He supports clients across statutory compliance, financial reporting, and income tax matters with a focus on accuracy, regulatory adherence, and disciplined execution.