Capital Gains Exemption: Why One Word Change in 2025 Can Alter Your Entire Tax Position.

In the world of Indian tax law, precision is everything. A single word sometimes even a comma — can redefine your entire tax liability. If you have ever claimed a capital gains exemption on the sale of property, business assets, or investments, you already know that the language of the law matters just as much as the numbers on your return.

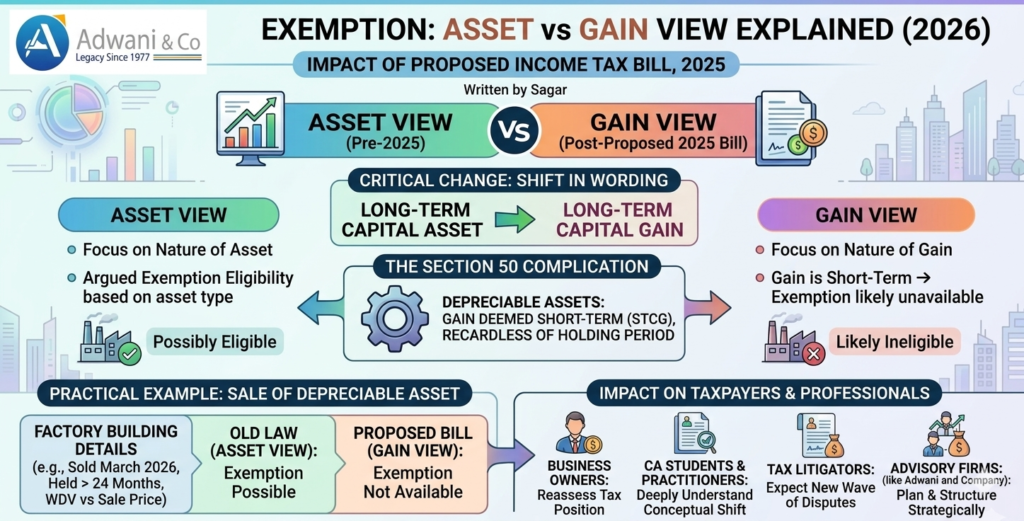

But here is something most taxpayers, and even many professionals, are not paying close enough attention to: the proposed Income Tax Bill, 2025, quietly changes one critical phrase that could reshape how capital gains exemption eligibility is determined across India.

The shift? From “Long-Term Capital Asset” to “Long-Term Capital Gain.”

At first glance, it looks like a cosmetic edit. In practice, it could trigger disputes, change eligibility, and force a complete rethinking of how depreciable assets, real estate holdings, and business investments are treated at the time of sale.

At Adwani and Company, led by Dr. Haresh Adwani, we have been studying the proposed bill closely. In this blog, we break down exactly what this change means, why it matters, and how you should prepare — whether you are a CA student, a tax practitioner, or a business owner planning your next asset sale.

Also Read:

Understanding the Core of Capital Gains Exemption in India

Before we dive into the 2025 changes, let us establish a solid foundation.

When you sell a capital asset whether it is land, a building, shares, or machinery the profit you earn is called a capital gain. Depending on how long you held the asset, this gain is classified as either short-term or long-term. And this classification determines whether you can claim a capital gains exemption under provisions like Section 54, 54EC, 54F, and others under the Income Tax Act, 1961.

Here is the traditional framework:

- Short-Term Capital Asset: Held for less than 24 months (or 12/36 months depending on asset type).

- Long-Term Capital Asset: Held beyond the specified period.

If the asset qualifies as long-term, you may be eligible for various capital gains exemption benefits — provided you meet the reinvestment and procedural conditions.

Simple enough, right? Not always.

The Section 50 Complication: When Holding Period Does Not Matter

This is where things get interesting, and where many taxpayers and even experienced professionals stumble.

Imagine you own a piece of machinery used in your business. You purchased it eight years ago. By any normal measure, it is a long-term capital asset. You sell it today at a profit.

Logically, you would expect this to be treated as a long-term capital gain, making you eligible for capital gains exemption.

But the law says otherwise.

What Section 50 Actually Does

Under Section 50 of the Income Tax Act, when you sell a depreciable asset an asset on which you have been claiming depreciation the gain is always treated as a short-term capital gain, regardless of how long you held it.

This means:

- You held the asset for 8 years → Still short-term gain.

- You held the asset for 20 years → Still short-term gain.

- The asset is clearly long-term by holding period → The gain is still deemed short-term.

This legal fiction has been a source of confusion and litigation for decades. The asset is long-term, but the gain is short-term. And your eligibility for capital gains exemption depends on which one the law prioritises.

As Dr. Haresh Adwani often explains to clients at Adwani and Company: “Section 50 is one of the most misunderstood provisions in Indian tax law. The holding period gives you a false sense of security. What matters is how the gain is characterised.”

The Traditional View: Focus on the Asset

Historically, the language of exemption sections like Section 54, 54EC, and 54F used the phrase “long-term capital asset.”

This meant the eligibility test was tied to the nature of the asset, not the nature of the gain.

Under this interpretation, some taxpayers and practitioners argued:

- The asset is long-term by holding period.

- Section 50 only deems the gain as short-term for computation purposes.

- The asset itself remains long-term.

- Therefore, capital gains exemption should still be available.

This “asset view” found support in certain tribunal decisions and was a popular planning strategy particularly for businesses selling old depreciable assets like buildings, vehicles, and plant and machinery.

However, this interpretation was not universally accepted, and it led to frequent disputes with assessing officers who took the opposite position.

The 2025 Shift: Focus Moves to the Gain

Now, here is the critical development.

Under the proposed Income Tax Bill, 2025, the wording in key exemption provisions is being changed. Instead of referring to a “long-term capital asset,” the new language refers to a “long-term capital gain.”

Read that again. The test is no longer about the asset. It is about the gain.

Why This One Word Changes Everything for Capital Gains Exemption

Let us revisit our earlier example:

- You sell a depreciable asset held for 8 years.

- Under Section 50, the gain is deemed short-term.

- Under the old law, you could argue the asset is long-term → exemption possible.

- Under the new law, the gain is short-term → exemption may not be available.

This is not a theoretical distinction. It has real financial consequences.

Consider a manufacturing business selling an old factory building:

| Parameter | Old Law | Proposed 2025 Bill |

| Asset holding period | 15 years (long-term) | 15 years (long-term) |

| Depreciation claimed | Yes | Yes |

| Gain classification (Sec 50) | Short-term gain | Short-term gain |

| Exemption test language | “Long-term capital asset” | “Long-term capital gain” |

| Exemption eligibility argument | Asset is long-term → possibly eligible | Gain is short-term → likely ineligible |

The financial impact? On a sale generating ₹2 crore in capital gains, losing capital gains exemption eligibility could mean an additional tax outflow of ₹30–40 lakh or more, depending on the applicable rate and surcharge.

A Practical Example: How This Plays Out in Real Life

Let us work through a detailed numerical example.

Scenario: Mr. Rajesh, a Delhi-based manufacturer, sells a factory building in March 2026.

- Original cost (2010): ₹80 lakh

- Written Down Value (WDV) as of sale date: ₹18 lakh (after years of depreciation)

- Sale price: ₹2.50 crore

Under Section 50: Capital gain = Sale price − WDV = ₹2,50,00,000 − ₹18,00,000 = ₹2,32,00,000

This entire amount is treated as short-term capital gain under Section 50, despite 16 years of holding.

Under old law (asset view): Rajesh could argue the asset is long-term and explore exemption under Section 54 (if reinvesting in residential property) or other applicable sections.

Under the proposed 2025 bill (gain view): The gain is short-term. The exemption test now looks at the nature of the gain. Rajesh may not be eligible for capital gains exemption at all.

Tax impact: At the short-term capital gains tax rate applicable to his income slab (say 30% plus surcharge and cess), Rajesh could face a tax liability exceeding ₹75 lakh on this single transaction — with no exemption route available.

This is exactly the kind of scenario where professional guidance becomes non-negotiable. At Adwani and Company, Dr. Haresh Adwani and his team regularly advise businesses on structuring asset sales to minimise such exposures before they become irreversible.

What This Means for Taxpayers and Professionals

For Business Owners

If you own depreciable assets — factories, office buildings, vehicles, plant and machinery — and you are planning a sale in the next few years, you need to reassess your tax position under the proposed framework. The capital gains exemption strategies that worked earlier may no longer be available.

For CA Students and Practitioners

This is a conceptual shift you must understand deeply. Exam questions and professional scenarios will increasingly test whether you can distinguish between the “asset view” and the “gain view.” More importantly, clients will expect you to know the difference.

For Tax Litigators

Expect a new wave of disputes. Taxpayers who have already planned transactions based on the asset view may find themselves in conflict with revenue authorities applying the gain view. Historical tribunal decisions supporting the asset view may lose relevance under the new statutory language.

How to Prepare for the Capital Gains Exemption Changes

Here are actionable steps recommended by the advisory team at Adwani and Company:

- Review pending asset sales: If you are planning to sell depreciable assets, evaluate whether completing the sale before the new bill takes effect could preserve your exemption eligibility.

- Restructure holdings: In some cases, transferring assets out of the depreciation block before sale (where legally permissible) may alter the tax treatment. This requires careful professional analysis.

- Document your position: If you choose to claim capital gains exemption under the current law, ensure your documentation and legal reasoning are watertight.

- Stay updated: The proposed bill is still under discussion. Track amendments, committee recommendations, and final enacted language. The Income Tax Department portal and the Ministry of Finance are your primary sources.

- Seek expert advice: This is not a do-it-yourself situation. The interplay between Section 50, exemption provisions, and the new bill’s language requires specialist interpretation.

The Bigger Lesson: In Tax, Every Word Counts

This entire discussion reinforces a fundamental truth about Indian tax law: the exact words in the statute matter more than assumptions or common sense.

As Dr. Haresh Adwani frequently reminds his team: “Tax planning is not about finding loopholes. It is about reading the law more carefully than anyone else in the room.”

The shift from “long-term capital asset” to “long-term capital gain” is a masterclass in legislative precision. One word changes the eligibility test. One word changes your tax liability. One word can mean the difference between a ₹0 tax bill and a ₹75 lakh tax bill.

Conclusion: Do Not Let One Word Cost You Lakhs

The proposed shift from “long-term capital asset” to “long-term capital gain” in the Income Tax Bill, 2025, is not a minor drafting change. It is a fundamental reorientation of how capital gains exemption eligibility will be determined for millions of Indian taxpayers.

Whether you are a business owner planning an asset sale, a CA student preparing for exams, or a practitioner advising clients, this is a development you cannot afford to overlook. The distinction between the asset view and the gain view will define tax outcomes worth crores of rupees in the years ahead.

Tax law rewards those who read carefully and plan proactively. It penalises those who assume yesterday’s rules still apply.

If you want expert guidance on capital gains exemption, asset sale planning, or any aspect of the proposed Income Tax Bill 2025, connect with Adwani and Company today. Led by Dr. Haresh Adwani, our team delivers the precise, strategic advice that protects your wealth and keeps you ahead of the law.

Schedule a consultation with Adwani and Company →

Frequently Asked Questions About Capital Gains Exemption

1. What is capital gains exemption under Indian tax law?

Capital gains exemption refers to provisions under the Income Tax Act (such as Sections 54, 54EC, 54F) that allow taxpayers to reduce or eliminate tax on capital gains by reinvesting the proceeds in specified assets within prescribed timelines.

2. How does Section 50 affect capital gains exemption eligibility?

Section 50 deems the gain on sale of depreciable assets as short-term, regardless of holding period. This can affect eligibility for capital gains exemption, especially under the proposed 2025 bill where the test shifts to the nature of the gain.

3. What is the difference between the asset view and the gain view for capital gains exemption?

The asset view focuses on whether the asset itself qualifies as long-term. The gain view focuses on whether the resulting capital gain is classified as long-term. The proposed Income Tax Bill, 2025, appears to shift the test toward the gain view.

4. Will the Income Tax Bill 2025 remove capital gains exemption for depreciable assets?

While the bill does not explicitly remove exemptions, the change in wording from “long-term capital asset” to “long-term capital gain” may make it significantly harder to claim capital gains exemption on depreciable assets where the gain is deemed short-term under Section 50.

5. How can I protect my capital gains exemption eligibility before the 2025 changes?

Review your asset portfolio, consider timing your sales strategically, and consult a qualified tax professional. Firms like Adwani and Company can help you evaluate your options under both the current and proposed law.

6. Where can I read the proposed Income Tax Bill 2026?

The proposed bill and related documents are available on the Income Tax Department’s official portal and the Ministry of Finance website.

7. Does capital gains exemption apply to all types of assets?

No. Each exemption section has specific conditions regarding the type of asset sold, the type of asset purchased, the timeline for reinvestment, and the amount eligible. Professional guidance is essential to determine applicability.

Author

CA.Dipesh Gurubakshani. He is a Chartered Accountant with professional experience in audit, direct taxation, and accounting advisory services. supports clients across statutory compliance, financial reporting, and income-tax related matters, with a strong focus on accuracy, regulatory adherence, and disciplined execution.